Your credit score is crucial if you’re hoping to take on funding for your business. While some lenders will work with borrowers with bad credit scores, you’re likely to get better terms when you have a healthy credit score.

September 2023 Update: Low credit scores is the number 1 barrier to small business financing this year. If you want to work with us to improve your credit score, learn more about the Skip 6 month credit assistance program.

Continue reading or watch the video version here.

If you have a high credit score, the lender will assume you will have no trouble paying back the loan. If your credit score is low, the lender will assume you may have a more challenging time paying back the loan. As a result, they will increase your interest rates to ensure they can recoup some of the loan, even if you can’t pay the total amount. Put simply, the better your credit score, the better your options for capital are.

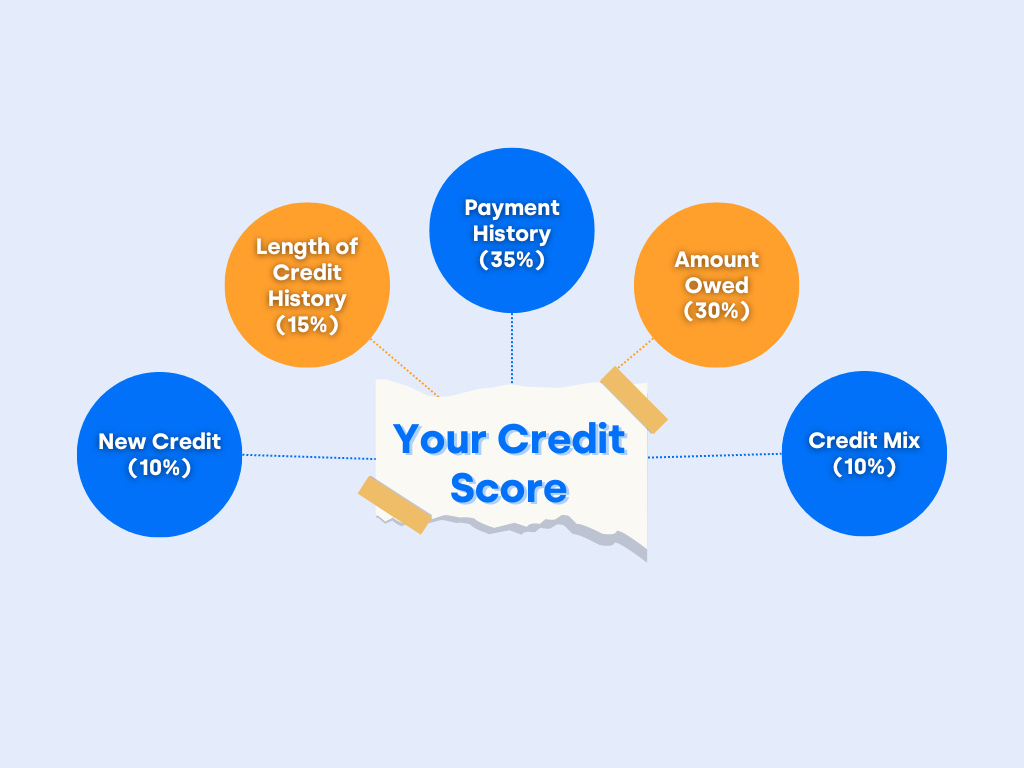

Before we dive in to our 10 tips, you should know that credit bureaus use the following information to calculate your credit score:

- Payment History (35%)

- Amount Owed (30%)

- Length of Credit History (15%)

- Credit Mix (10%)

- New Credit (10%)

📌 If you are looking to improve your credit score to get funding for your business, please give us a call! We have credit repair specialists on board to dive right in. Plus, we've helped people with very poor credit still get funding. There are a lot of options out there that we can help connect you with. Book a 1-1 call here.

Here are our 10 tips for improving your credit score

1. Enroll in automatic payments

Since payment history is your number one priority when improving your credit, automatic payments will help prevent things from slipping through the cracks. Your bank should detail how to do this on your account homepage.

2. Payoff collections

If you have missed payments and have been sent to collections, then simply taking care of this can do wonders for your credit score. You can contact your creditor directly to make payment arrangements.

3. Negotiate settlement offers

Once your debt goes into collections, you may not necessarily need to pay off the full amount. You can negotiate a settlement agreement to pay off a smaller portion of the original amount owed and settle the debt as "paid."

4. Pay down your balances

You can sell things or start a side hustle. You can also see an increase in your credit score by making extra, separate payments each month instead of one large payment.

5. Keep your oldest credit card or credit account active

Canceling your oldest credit card is one of the biggest mistakes you can make when it comes to your credit score. Perhaps pay a bill with it and pay it off monthly to ensure you’re using it, but never cancel it.

6. Diversify your types of credit

You can create what's called a "credit mix" by utilizing different types of credit each month. Having debt via a credit card, car loan, student loan, or home loan increases your credit mix as long as you pay your monthly balance on time. You can do this if your credit score is already good and you want to maintain it.

7. Review your credit report often for inaccuracies

Over 80% of credit reports contain inaccurate information such as the spelling of the applicant's name, incorrect address, etc. This misinformation should be removed immediately. Once this information is removed, any accounts associated with the incorrect information can be removed.

8. Ensure all outdated information has been removed from your credit report

Items over 7 years should fall off, but this isn't always the case. To remedy this, you can send a letter to the credit bureau(s) to request they remove old debts from your credit report. Make sure to include any relevant supporting information with your letter.

Once you take this step, the bureau will open an investigation and ask the creditor reporting the debt to verify it. If they can't, the debt will come off your report.

9. Refrain from applying for any unnecessary new credit

Hard inquiries remain on your credit for 2 years. Try to limit the number of hard inquiries to only necessities.

10. Try the "snowball" method

If you have a lot of credit card debt with high utilization, trying paying it down using the "snowball" method. This entails focusing on paying off one card at a time using extra payments, while making the minimum payment on your other cards. This will result in a faster increase of available credit compared to paying a little extra on all cards at the same time.

Once you get a card under 30%, your score will increase. Once a card is paid, use the additional money to focus on the next card.

What to do if you don’t have credit

If you don’t have any credit and are trying to establish credit, you have a few options.

One popular choice is a secured credit card. These cards require a "deposit" in the amount of your credit limit.

Another good option is store credit cards. Department stores, home improvement stores, and office supply stores are a great place to start.

Lastly, you can build your credit by showing that you pay your rent, utilities, and phone bill on time. Experian has a way for you to do this called Experian Boost, and there are other companies out there that can help with that too.

💡 Want to learn more about increasing your credit? Watch our full video here.

📌 If you decide you want 1-1 help with credit, business funding and more, book a free call with our team to learn more about our memberships.